Fixed Rate vs Adjustable Rate Mortgages in California

What is the difference between fixed and adjustable rate mortgages?

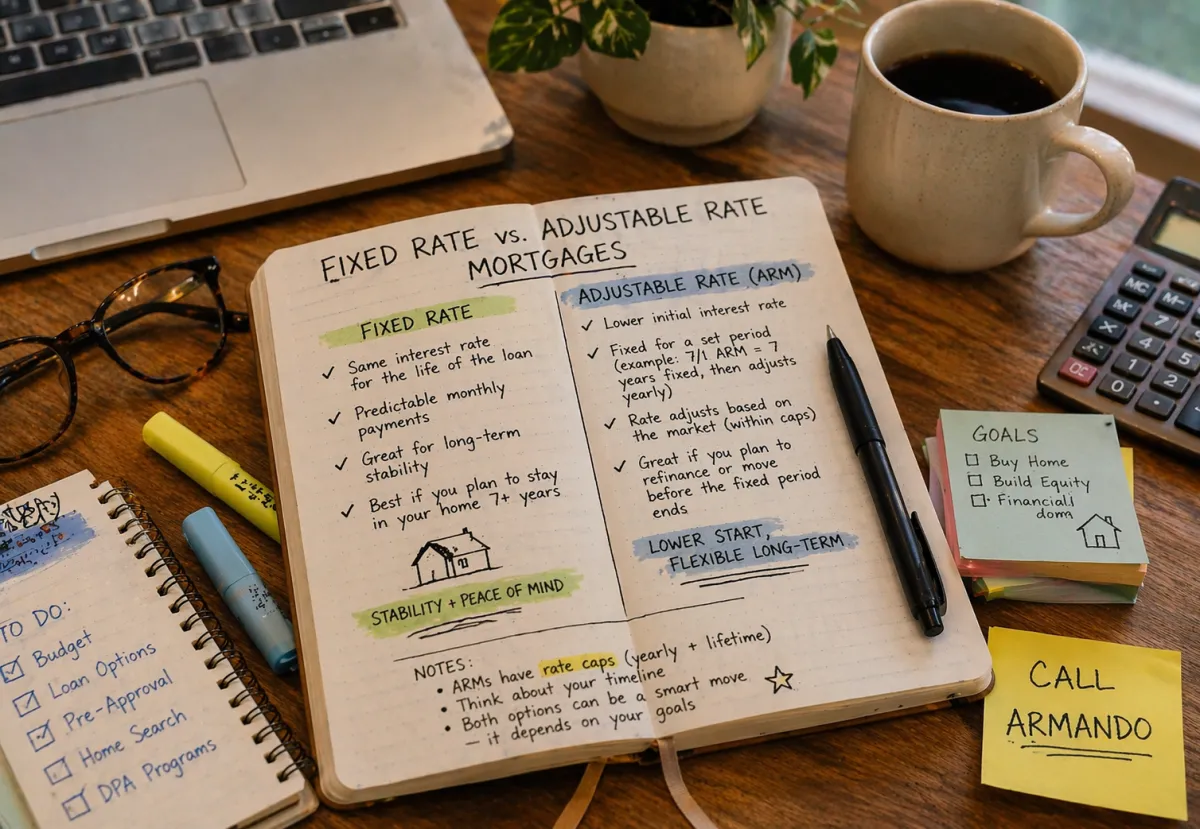

A fixed-rate mortgage keeps the same interest rate for the life of the loan. An adjustable-rate mortgage starts with a fixed period, then adjusts based on the market.

Both options are used every day in California. The right one depends on your timeline and how long you plan to keep the loan which is why talking to a lender early changes how you approach these decisions.

Why do adjustable-rate mortgages have a bad reputation?

Adjustable-rate mortgages got a bad name during the 2008 meltdown because the adjustments were aggressive. Rates jumped quickly and payments increased in a way many borrowers weren’t prepared for.

Back then, some loans were structured in ways that didn’t give buyers much protection.

I’ve talked to a lot of homeowners who still remember those stories. It’s one of the first concerns that comes up when we bring up ARMs.

What people don’t realize until we break it down is that today’s adjustable-rate loans are very different.

Are adjustable-rate mortgages safer today?

Yes, today’s adjustable-rate mortgages are structured with caps that limit how much the rate can increase. There are limits on how much the rate can adjust each year and over the life of the loan.

Most ARMs today follow a clear structure. You get a fixed rate for an initial period, then adjustments happen at set intervals with defined caps.

For example, a 7/1 ARM gives you a fixed rate for 7 years. After that, the rate adjusts once per year based on market conditions, but within set limits.

I had a client recently who assumed their payment could double overnight. Once we reviewed the caps, they realized the adjustments are controlled and predictable.

A real mistake is comparing today’s ARMs to what happened in 2008 without understanding how the guidelines have changed.

What is a hybrid ARM and why are buyers using it?

A hybrid ARM is a loan that starts with a fixed period and then adjusts later. The 7/1 ARM is one of the most common options right now.

In today’s market, many buyers don’t plan to keep the same mortgage long term. They might refinance, move, or upgrade before the fixed period ends.

That’s why a 7/1 ARM can make sense. You get a lower rate upfront during the years you’re most likely to keep the loan.

An anonymous client chose a 7/1 ARM because they knew they wouldn’t stay in the home longer than 5 to 7 years. That decision gave them a lower payment without taking on long-term risk.

What people don’t realize until they’re in it is how often homeowners change their loan before 30 years.

When does a fixed-rate mortgage make more sense?

A fixed-rate mortgage is best for buyers who want stability and plan to hold the loan long term. Your payment stays the same, and there’s no concern about future adjustments, which can help buyers better manage costs that first-time homeowners often overlook.

I still recommend fixed loans all the time. It comes down to your comfort level and your plan.

One Google review says it well: “Armando helped us understand both options so we could choose what fit our situation.”

Final Thoughts

There’s no one size fits all when it comes to mortgage. Fixed and adjustable loans both have a place depending on your timeline.

The key is understanding how long you’ll keep the loan and how each option works before you decide.

For more info, join my email list.