The Homebuyer’s Corner

Fixed Rate vs Adjustable Rate Mortgages in California

Written by Armando Novelo, NMLS 237243, a mortgage loan officer in West Covina with over 20 years of experience helping Southern California buyers.

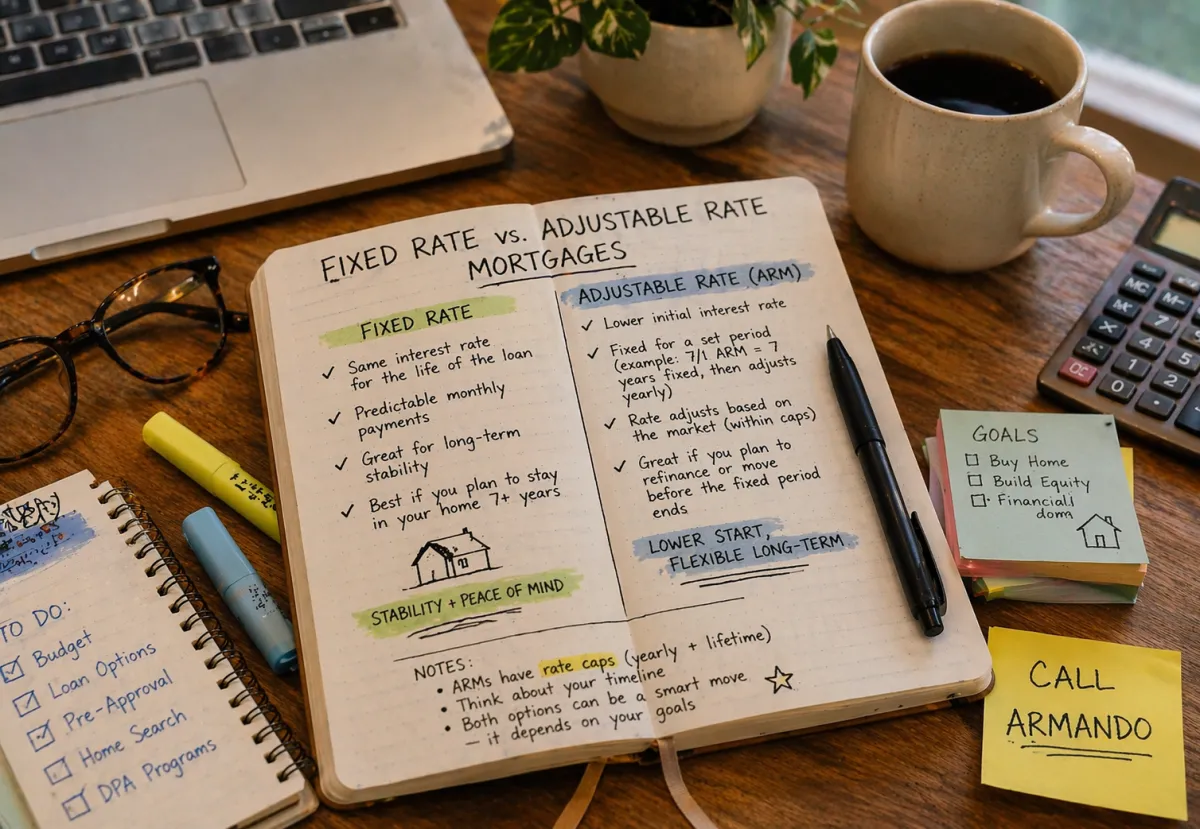

A fixed-rate mortgage keeps your interest rate the same for the life of the loan. An adjustable-rate mortgage starts with a fixed period and then adjusts based on the market after that period ends. Both are legitimate options. The right one depends almost entirely on how long you plan to keep the loan.

Most buyers default to a 30-year fixed without ever asking whether it is actually the best fit for their situation. Sometimes it is. Sometimes it is not. That decision is worth a real conversation before you commit to it.

What a Fixed-Rate Mortgage Gets You

Simple. Predictable. The same principal and interest payment every single month for 30 years, or 15 if you go that route. Your rate does not move regardless of what the market does. If rates go up after you close, you are protected. If rates go down, you can refinance.

Right now in California, 30-year fixed rates are averaging in the mid to upper 6 percent range. On an $800,000 loan at 6.5 percent, your principal and interest payment is around $5,060 a month. That number does not change. Ever. Until you pay it off, sell, or refinance.

That stability is worth a lot to a lot of buyers, especially if you are planning to be in the home long term and you want your housing costs to be completely predictable.

What an Adjustable-Rate Mortgage Actually Is

This is where most buyers shut down because of what they remember about 2008. Understandable. But the product has changed significantly since then and comparing today's ARM to what happened in the mid-2000s is not an accurate comparison.

Here is how a modern ARM works.

You get a fixed rate for an initial period, typically five, seven, or ten years. After that, the rate adjusts once per year based on a market index, the SOFR rate, plus a lender margin. But here is the part most people do not know. There are caps built into the loan that limit how much the rate can move.

A typical ARM today has a cap structure written as something like 2/1/5. That means the rate cannot go up more than 2 percent at the first adjustment, no more than 1 percent per year after that, and no more than 5 percent total over the life of the loan from where it started. Those caps are legally binding. Your rate cannot just spike to whatever the market is doing.

The most common option right now is the 7/1 ARM. Fixed for seven years. Adjusts once per year after that within those caps.

What the Actual Payment Difference Looks Like

This is the conversation most buyers never get to because the discussion stops at "fixed is safer."

Let's use an $800,000 loan as an example, which is a reasonable starting point for a single family home purchase across much of the San Gabriel Valley right now.

At a 30-year fixed rate of around 6.5 percent, your principal and interest payment is approximately $5,060 per month.

A 7/1 ARM in California right now is running roughly 0.25 to 0.5 percent lower than the 30-year fixed. At 6.1 percent on the same $800,000, your payment comes down to around $4,850 per month. That is about $210 less every month, or roughly $2,500 per year, for the first seven years before any adjustment happens.

Over those seven years, that gap adds up to around $17,500 in your pocket versus the fixed. If you sell or refinance before year seven, which a significant portion of California homeowners do, you never experience a single adjustment.

That is not reckless. That is math.

When the ARM Makes Sense and When It Does Not

The ARM makes sense when you have a clear reason to believe you will not keep the loan past the fixed period. You are buying a starter home with a realistic plan to upgrade in five to seven years. You know you are relocating for work within that window. You are planning a significant life change that would trigger a sale or refinance.

I have worked with buyers in the San Gabriel Valley who chose a 7/1 ARM knowing they were in a transitional phase. They got a lower payment during the years they needed it most, and they moved before the rate ever touched an adjustment. That decision made sense for their situation.

The ARM does not make sense when you genuinely plan to be in the home for the long haul and you want to sleep at night knowing your payment is never going to change. There is real value in that peace of mind and it is worth the slightly higher rate for a lot of people. Especially buyers who are stretching to afford their payment and have no cushion if anything changes.

The mistake is not choosing an ARM or choosing a fixed rate. The mistake is choosing one without understanding why.

The 2008 Question Everyone Asks

When I bring up ARMs, someone in the room always says "but what about 2008."

What happened in 2008 was that a lot of loans were structured with very short fixed periods, aggressive adjustment schedules, and no meaningful caps. Some were interest-only for the fixed period, meaning buyers were not paying down any principal. When those loans adjusted, payments jumped dramatically and many borrowers could not absorb the increase.

Today's ARM guidelines are completely different. The caps are real. The adjustment schedules are reasonable. The products are structured to be survivable even if rates move.

That does not mean an ARM is right for every buyer. It means the comparison to 2008 is not an accurate way to evaluate the product today.

Which One Is Right for You

Ask yourself one question honestly. How long do I actually plan to keep this loan?

If the answer is more than ten years, a 30-year fixed is probably the right call. Lock in your rate, know your payment, move on with your life.

If the answer is five to seven years or you are genuinely unsure, the ARM deserves a real look. Not as a risk move. As a financial decision based on your actual timeline.

The rate environment in California right now means the spread between fixed and adjustable is real and the savings during the fixed period are meaningful. Whether those savings are worth the flexibility trade-off depends on your situation specifically, not on a general rule.

This is the kind of conversation I have with buyers every week. It is not complicated once you lay out the actual numbers for your specific loan amount and timeline.

Armando Novelo, NMLS 237243, is a mortgage loan officer at Super Mortgage Bros, powered by Golden Empire Mortgage. He has been helping Southern California buyers since 2002. His office is located in West Covina, CA.

For more info, join my email list.

Article Published: April 8, 2026

Links

Contact

Armando Novelo

NMLS 237243

Super Mortgage Bros

1900 W. Garvey Ave S. #100

West Covina, CA 91790

Phone: (626) 200-1838

I agree to be contacted by Super Mortgage Bros via call, email and text. To opt out, you can reply “stop” at any time or click the unsubscribe link in the emails. Message and date rates may apply.

Message frequency varies

© 2026 Super Mortgage Bros. Super Mortgage Bros. | All Rights Reserved | Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act. Golden Empire Mortgage, Inc. ("GEM") [NMLS ID No. 2427] is a California corporation whose principal business office is located at 1200 Discovery Drive, Ste. 300, Bakersfield, California 93309. GEM is a residential mortgage lender and servicer Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act. under license no. 413-0360. https://www.nmlsconsumeraccess.org